The holiday season is a time of joy, celebration, and, often, a surge in spending.

As the holiday cheer fills the air, it’s easy to get caught up in the excitement and overspend – and that’s where some folks opt for a holiday loan.

However, there’s a smarter way to navigate the holiday season without breaking the bank.

In this guide, we’ll explore the ins and outs of holiday loans, their potential benefits and drawbacks, and alternative options to fund your festivities.

By understanding the mechanics of holiday loans and considering other financial options, you can make informed decisions and enjoy the holiday season without worrying about overwhelming debt.

What is a Holiday Loan?

An expense-related personal loan for the holidays is known as a holiday loan.

Banks, credit unions, and internet lenders all provide these loans.

A holiday loan often offers a predictable repayment plan ranging from six months to five years, with:

- a fixed interest rate

- fixed monthly payment

- defined loan period

To offset the costs of making the loan, certain lenders may impose an upfront fee.

You could be able to borrow up to $5,000, depending on the lender, to buy presents for loved ones or to cover additional holiday costs like celebratory meals and travel.

How Holiday Loans Work

Most holiday loans, like many personal loans, are unsecured and don’t call for security as long as you fulfill the requirements of the lender.

However, some lenders could demand that you use collateral, such as a car, to receive larger loans. Your interest rate, the size of the loan, and ultimately your monthly payment are often influenced by your income and credit rating.

By supplying a few pieces of financial information, you may pre-qualify with some lenders for a holiday loan without it having any effect on your credit score.

Pre-qualifying gives you the opportunity to examine several loan offers based on their:

- terms

- APRs

- monthly payments

- origination costs, which may be as much as 10% of the loan amount

The total cost of the loan is impacted by each of these expenses.

If you’re a member in good standing, Christmas loans from credit unions can be the most alluring choice out of the ones offered. Some credit unions have more affordable interest rates or don’t verify your credit.

How Much Does a Holiday Loan Cost in Interest?

There are several variables that affect how much interest you will pay on a holiday loan.

Scenario 1: $5,000 loan with origination fee.

Consider you want a $5,000 loan to pay for presents and trips.

This could look like a holiday loan for 24 months with an APR of 19% and an initiation charge of 3.7%.

You would only receive $4,815 if your lender took the origination charge out of your loan at the start, which might not be enough to cover all the costs you had budgeted for.

So then you ask for a $5,200 loan to cover this amount.

- Monthly payment: $262.12

- Loan period: 24 months

- Interest paid over term: $1,091.00

- Total paid over term: $6,291.00

Scenario 2: $5,000 loan without origination fee.

You may save money by looking around for a lender who doesn’t charge an origination fee.

- Monthly payment: $252.04

- Loan period: 24 months

- Interest paid over term: $1,049.03

- Total paid over term: $6,049.03

Scenario 3: $5,000 loan for 36 months.

Another approach to reduce your monthly payment is to extend the loan period. Doing so will result in higher overall interest costs.

Take into account our $5,000 loan with a 19% APR and no origination charge.

- Monthly payment: $183.28

- Loan period: 36 months

- Interest paid over term: $1,598.08

- Total paid over term: $6,598.08

Scenario 4: $5,000 loan for 12 months.

The greatest interest may be saved by paying off the loan early, but doing so will increase your monthly payment.

- Monthly payment: $460.78

- Loan period: 12 months

- Interest paid over term: $529.39

- Total paid over term: $5,529.39

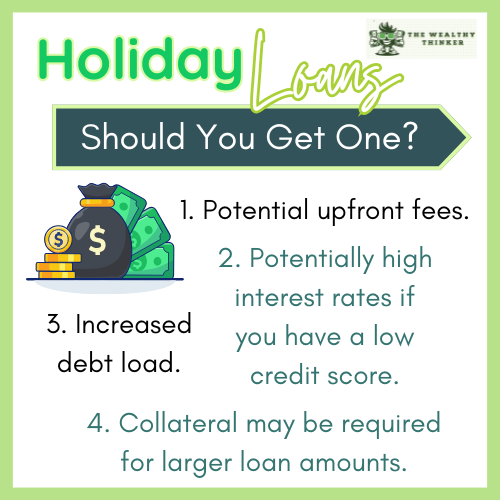

Why You Should Not Take a Holiday Loan

1. Potential upfront fees.

Some lenders could impose an origination fee, which might raise the total amount of interest you have to pay as well as the amount you have to borrow.

2. Potentially high APRs if you have a low credit score.

Holiday loan APRs (Annual Percentage Rate) are frequently determined by your credit score.

With a poor credit score, you could only be eligible for loans with higher APRs. This would raise your monthly payment and make the loan harder to repay.

3. Increased debt load.

Your debt load increases if you borrow money for Christmas gifts.

Your credit score may be impacted and your APR for future credit cards and loans may go up if you have a lot of debt.

4. Collateral may be required for larger loan amounts.

You could be asked to provide collateral by some lenders, especially for large loan sums.

Accepting the loan puts you at danger of losing your asset if you can’t keep up with the payments.

6 Alternatives to a Holiday Loan

1. Personal Line of Credit.

A personal line of credit is a sum of money from which you have unlimited access for a certain length of time.

A line of credit, as opposed to a loan, allows you to use a portion of the available funds. This might assist you limit your holiday expenditures.

Line of Credit vs. Credit Card? The Key Differences & Benefits

2. P2P Loan.

P2P loans (Peer-to-peer loans) are offered by companies or even by other customers through online marketplace platforms.

While lower than credit card interest rates, they might be higher than those on a vacation loan. A P2P loan may be easier to obtain authorization for than a bank loan for those with recent credit histories.

3. Credit Card.

When you can benefit from a special APR deal, using a credit card may be more advantageous than getting a holiday loan. You may, for instance, use a credit card with a lengthy 0% APR term to pay off the debt over time with no interest.

Some credit cards enable you to get a low-interest, fixed-rate loan with a lower APR than for typical purchases by using your current available credit.

As you are using your unused credit, you won’t need to apply for a new loan. You might be able to avoid costs with this choice.

Balance Transfer Cards: Should You Consider Getting One?

4. Reduce Your Holiday Budget.

Limit your list to ensure that you can do all of your shopping with the money you have.

Making cuts to your Christmas spending may include purchasing fewer gifts or doing less shopping, but it will save you from accruing additional debt.

You may also use creativity when choosing your presents. Think about giving handcrafted products, economical activities, and other possibilities that are free or inexpensive.

5. Take on Temporary Holiday Work.

Many retailers look for extra help over the holidays.

Consider applying for a temporary holiday job or picking up extra shifts at one you already have. Bringing in extra cash would give you the flexibility to spend a little more on gifts without having to borrow money.

6. Use Credit Card Points.

Depending on the rewards program for your credit card, you might be able to use your points to pay for any presents you’ve already charged to your card as a statement credit or deposit them into your bank account.

By exchanging your rewards into gift cards, you might be able to get more value out of your points. Depending on your card, you may give them as presents or use to buy goods from merchants.

Check to see whether you may use your travel points in place of a vacation loan to pay for your travel expenses.

Key Takeaways on Getting a Holiday Loan

A holiday loan is a kind of personal loan that can be used to pay for travel or Christmas presents.

Depending on the lender and the state of your credit, there may be differences in:

- loan terms

- interest rates

- fees

- monthly payments

Instead of taking out a vacation loan, think about other options that can enable you to borrow money for less or possibly not at all.

Editor’s note: This article was originally published Dec 20, 2022 and has been updated to improve reader experience.